Weighing a CRE ‘Cash-In’ Refinance: A Case Study

For various reasons, ‘cash-in’ refinances have seen an uptick in prevalence in commercial real estate. I plan to discuss refinance risk and whether or not a cash-in refinance is worth it in the context of a multifamily investment facing an imminent refinance that would require more cash from investors.

Contents

Avoiding Refinance Reliance

Underwriting a refinance is unnecessarily risky for stabilized properties, which need only cosmetic upgrades and qualify for traditional agency or bank financing. Successful refinances depend on three critical factors:

Executing your business plan

Steady property valuations (ideally appreciating)

Robust capital markets

You only control #1 as an operator, while #2 and #3 are left to the broad market and macroeconomic landscape. Furthermore, a cash-out refinance projection will likely inflate IRRs and equity multiples and could exaggerate the investment thesis.

Note: This is a big reason Tactica's Value-Add Model doesn't include a refinance toggle (as this tool is ideal across the spectrum of newer "Class A" properties," to "Class C" properties.

Underwriting refinance proceeds should only be considered when the business plan requires short-term debt (sometimes floating rate), such as construction or bridge loans. You'd use these types of financing arrangements in the following projects:

In this article, I touch far more on the risks of banking on refinance proceeds in proforma underwriting.

Reasons For 'Cash-In' Refinance

A ‘cash-in’ refinance means the investor needs to come to the table with more money to continue their investment hold. Failure to inject more cash could create immediate loss, sometimes up to 100% (total equity loss). If the funds come from passive (LP) investors, this will come as a “capital call” or “additional contributed capital.”

Some of the most common reasons for this in 2024 are due to:

Balloon Payments Coming Due

Deleveraging of Lending Institutions

Valuation Declines (Cap Rate Expansion)

Weakening Property Operations

Ballon Payments

Commercial loans commonly have a term between 5 - 10 years. At the end of the term, the loan is expected to be paid down in full (the balloon).

Investors often use bridge or construction financing for shorter periods, intending to refinance into permanent, amortizing mortgages upon completing a repositioning or a new development.

A mortgage balloon is nothing new. Investors are used to getting new financing at least once every ten years. Thousands of real estate loans will come due yearly and be replaced via a refinance or taken out by a sale.

However, ballooning loan payments are more problematic today as we find ourselves in correction territory in commercial real estate. The capital markets vastly differ from the last time groups sought financing, which will likely cause friction when recapitalizing the project.

Deleveraging of Lending Institutions

Many lenders have slowed down their funding, and active ones today aren't giving loans with 80% LTV as frequently. If you purchased a property five years ago, and your loan is coming due, this could be problematic if the same lender is only willing to give you 65% LTV today.

Example: You bought the property five years ago for $10,000,000; the loan amount was $8,000,000 and full-term interest only. Today, the property is valued at $12,000,000, but the lender is only willing to give you 65%, or $7,440,000.

65% x $12,000,000 = $7,440,000

If you moved forward with that financing, you'd need to bring $560,000 in new cash to pay off the old loan.

$7,440,000 - $8,000,000 = -$560,000

Valuation Decline

In the last scenario, the property increased in value by $2,000,000 over the past five years.

$12,000,000 - $10,000,000 = $2,000,000

But what if the property would have lost value? This decline is happening to many properties purchased between 2020 and 2021.

If the $10,000,000 property is now worth $9,000,000 and the lender is only willing to give 65% LTV, you'd need to bring an additional $2,150,000 of cash into the project.

$9,000,000 x 65% - $8,000,000 = -$2,150,000

Weakening Property Operations

The triple whammy would be operations suffering (decreasing NOI). Weaknesses could be a high economic vacancy, inflated expenses, and overall profit lacking initial prognostications.

Lenders are constrained by both LTV and debt coverage (DSCR). A lender might require a 1.25 DSCR. If the 65% LTV results in a 1.17x DSCR, they would need to back off the loan proceeds until the DSCR is equal to or greater than 1.25.

For example, the lender must move LTV down to 60% in this scenario. Now, you'd need to bring $2,600,00 to the closing table to take out the $8,000,000 loan.

$9,000,000 x 60% - $8,000,000 = -$2,600,000

The scenarios above represent a spectrum of unexpected hurdles that could have taken place between financing periods. The next step will be to examine whether or not it makes sense to put more money into the deal.

'Cash-In' Refinance Analysis

Wise investors won't chase bad money with good money. It's essential to evaluate the market, the property, the operations, and the future outlook to see if putting more money into the deal will help you recoup your initial investment and earn a return on the second equity contribution.

A rational sponsor/investor shouldn’t make the mistake of requesting more money for a project with a minimal chance of success and will weigh options to maximize the return of investor capital, even when the outlook is bleak.

Sales Comps Review

First, you must understand what properties are selling for in the market. I show you how to do this in the article "Determining a Good Cap Rate."

Ultimately, you need an estimate of what the investment property could fetch if you sell it today. Suppose you purchased the property at a 3.5% rate in 2021, and the same type of properties are trading at 5.5% cap rates today. In that case, it's doubtful you'll ever recoup your initial investment, even if you buy more time with a ‘cash-in’ refinance.

On the flip side, if you had a "good buy" back in 2021 and purchased a property off-market at a 5.5% cap, and now the market cap rate is 6%, there's a chance your project is salvageable.

I'll dive into some actual numbers, but before we get to deep in the weeds, it's paramount to understand what your property is worth compared to:

The original purchase price

The outstanding loan balance is

Investing more money into the deal to recoup initial losses will likely be an uphill climb if the existing loan is worth more than the property.

'Cash-In' Refinance Case Study

I'll be using Tactica's Multifamily Redevelopment Model for this analysis.

Let's say we invested in a project as an LP in early 2022. Although the market has shifted dramatically, the business plan was executed flawlessly two years into the investment hold.

We originally paid $16,000,000 for an 88-unit apartment building. The plan was to renovate all units and achieve a $430 premium (which was accomplished).

All revenue and expense assumptions tie out perfectly with the original proforma projections.

Note: Realistically, the property will overachieve or underachieve proforma projections, and you may have to create a hybrid hold vs. sell analysis that includes historical performance and proforma projections.

Two years ago, we paid a 4.02% cap on historical T3/T12 financials, intending to achieve close to a 6% yield-on-cost upon completing renovations.

We financed the project with 80% LTC bridge financing (the financing covered a portion of the renovation and the purchase).

The rate in early 2022 was 3.50%. However, the bridge debt was floating-rate, and we used a rate cap where the worst-case scenario would be interest payments increasing to 4.50% (the max exposure). That's what we underwrote above.

Today, we need to refinance. The renovation is complete, the property is stabilized, and we need to get out of this bridge loan.

Financing terms are much less favorable today. Lenders are offering less leverage, and rates have climbed drastically. The best financing offer would include 65% LTV and a 6.5% interest rate.

Furthermore, this sub-market has seen a significant correction in valuations. While a 4% cap was an aggressive purchase two years ago, conservative market cap rates are between 6.00% and 6.25% today. When determining loan proceeds, the lender's loan proceeds will use a 6.25% cap rate and apply it to the stabilized NOI.

Thankfully, today's valuation at a 6.25% cap is still worth more than the outstanding loan amount ($15,203,722 vs. the original loan amount of $13,865,500).

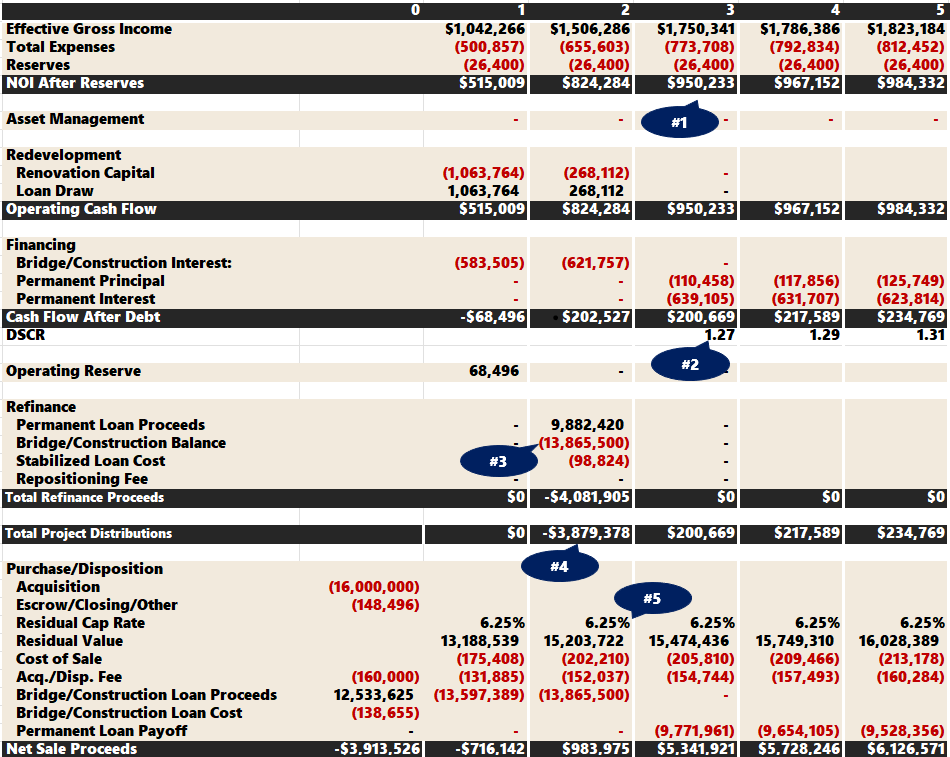

Let's take an in-depth look at how the numbers shake out.

You can see some labels of items I want to discuss in the image.

The stabilized NOI is $950,000. The operator has achieved the proforma rents and should hit these benchmarks by the end of Year 3. Rents will continue to increase at 2% after that, per the proforma projections.

The DSCR is 1.27 once new financing is in place, meeting the lender’s requirement.

The original bridge loan of $13,865,500 is much larger than the new permanent financing amount of $9,8882,420.

The difference between permanent financing and the bridge loan plus financing fees, minus the operating cash flow of $202,527, is a -$3,879,378 shortfall and is the "cash-in refinance/capital call" amount.

The current cap rate in the market is conservatively 6.00% - 6.25%. I continue to run it at 6.25% for the duration of the proforma. While cap rates will hopefully compress again, we don't want to bank on it.

Now, let's take a look at the return metrics.

Again, I have labels pointing out a few things.

The equity multiple crosses 1.0x at the end of Year 7. Assuming the business plan continues as estimated, breaking even on your initial investment and cash-in refinance contributions would take five more years.

The cash-on-cash return is 2.50%. It's a pretty pedestrian yield, considering you can get 5.00% risk-free at writing.

Opportunity Cost of Capital Call

If you partake in the capital call, consider it a separate investment. There's an opportunity cost with putting more money into the deal. Let’s walk through that thought process. We need to think through two scenarios:

Complying with the Capital Call

Forgoing the Capital Call

Complying with the Capital Call

Remember, in our scenario above, we are LP investors and put $100,000 into this project two years ago. Let’s take a quick look at the partnership distribution model (in this instance, a simple interest waterfall).

You can see that when the refinance happens in Year 2, we’d go negative $3,879,378. This is nearly the same amount as we initially contributed in Year 0. Off to the right, the GP would be responsible for 10% of that amount and the LP 90% (per the contribution percentages stipulated on the top-right).

We’d need to match our initial equity contribution or another $100,000. We'd be in for $200,000 after the cash-in refi.

Year 0: -$100,000

Year 2: - $100,000

Total Investment = -$200,000

If we put in $200,000 and the proforma played out as in the image above, in Year 7, we could sell, we'd be at a 1.09x equity multiple, equating to $218,000 or an $18,000 profit.

$200,000 x 1.09 = $218,000

Forgoing the Capital Call

But what if we took that $100,000 and instead did something else with it? Like buying stocks (S&P 500), a REIT, or investing in another private real estate project?

If you forgo the capital call, your ownership stake will be diluted. Because the cash-in refinance amount is double the initial equity invested, if you didn't participate in the capital call, your ownership would be cut by 50%.

So when the property sells in Year 7, your return would be:

$100,000 x 1.09 x 50% = $54,500

Total Loss = $45,500

Then let's say your next $100,000 made 10% per year in the S&P 500 for five years

$100,000 x 1.10^5 = $161,051 or $61,050 in profit

$61,050 gain + $45,500 loss = $15,550 in total profit

In this instance, there's no considerable difference in monetary gain by participating in the capital call vs. doing it with an S&P 500 index fund instead over a 7-year horizon.

$18,000 if you stay in the real estate deal for the additional $100,000

$15,500 if you decline the capital call and instead invest $100,000 in the S&P compounding at 10% annually

In this specific scenario, I would choose the real estate. Here's why:

The operator was executing but was caught in a challenging macro environment. They can't control cap rates and lender behavior, but they did see an opportunity to improve property operations, and they have done that. I would expect them to continue to meet expectations in future years.

It's slightly more profit (albeit not material) but with more tax benefits.

I'd want to support an operator I trust and would invest with in the future.

If there is some cap rate compression, this project still could overachieve (but I’m not counting on it).

Ultimately, I'd choose real estate because the operator was executing well and excelled in the arena she could control.

This decision is much more of an art than a science. If there’s distress in the market and asset valuations are down, would putting the $100,000 in another private real estate project make more sense and provide more upside?

Execution is the Ultimate Question

If I were pondering participating in a capital call, and the actual financial performance was worse than the initial projections, I would move on from the project and put my cash elsewhere. Chasing losses can be dangerous, and if I have lost faith in the operator, I will cut my losses and move on.

For example, let’s pretend the operator in our scenario above underestimated the rent premium by 50% ($215 per unit instead of the $430 initially underwritten).

Now, the returns are even more abysmal. In Year 10, the equity multiple would climb to only 0.47.

Had I participated in the capital call, I’d have received only $94,000 back

$200,000 x 0.47 = $94,000

Total Loss = $106,000

The additional investment would have been much more effective elsewhere.

If the sponsor didn't execute up to this point, I wouldn't be confident they would in the future, and I wouldn't chase bad money with good. It's essential to run the scenarios to be sure.

Summarizing Cash-in Refinance

A 'cash-in' refinance is an investment setback commercial real estate investors may face in a rising interest rate environment due to:

Balloon Payments Coming Due

Deleveraging of Lending Institutions

Weakening Property Operations

Valuation Declines (Cap Rate Expansion)

If you find yourself weighing whether a cash refinance is a prudent investment, you must have a firm understanding of the sales comps in your market and be able to run through underwriting scenarios that will tackle the likelihood of getting paid back in whole or, hopefully, profiting.

There is an opportunity cost to putting more cash into a real estate investment; there are instances where your money would be better invested elsewhere.