Do Apartment Developers Have an Underwriting Blind Spot?

I've analyzed many newly developed multifamily projects during their lease-up. A recurring theme has emerged when reviewing the numbers revolving around property tax underwriting.

Contents

Property Taxes After Sale

Developers often forget how future property tax increases could affect the residual sales proceeds. Because it's "the next group" who will own the property and deal with a more considerable tax burden, increasing property taxes falls outside the developers' scope (and outside of their proforma projections).

Realistically, this is flawed as the developer SHOULD account for the next owner's burden as it will impact what they can pay for the asset. I dedicated an entire tab in the Multifamily Development Model to property tax sensitivity.

Property Tax Comps

The typical process that I observe is that the developer would use a tax comp methodology:

Find comparable apartments in the direct vicinity of their project

Choose the projects that had similar finish levels, comparable amenity packages, and similar rents

Underwrite their project's stabilized real estate tax expense in line with these comps on a per-unit basis

If they were developing the project with the intent to hold it long-term, I would have no issue with this rationale. The problem lies in the fact that, in many instances:

The developer wants to sell once the property is stabilized (or pre-stabilized).

The development will sell for more than the assessment levels of any comps.

Tax comps have yet to sell.

There are comparable properties in the taxing authority's jurisdiction that have been sold and reassessed and have materially higher property tax (on a per-unit basis) than those used as comps.

The buyer of the development has to bear this future tax liability. Therefore, they need to discount the NOI when underwriting a potential acquisition of a new apartment complex. This discount is typically done with a capitalization rate (cap rate) adjustment that can drastically impact the developer's residual sales price.

Development Case Study

Let's look at a theoretical 180-unit building constructed in Minneapolis, MN. We will assume that construction will start on 1/1/2023 and last 14 months. Lease-up assumptions are the following:

We will assume that the developer sells the project on the 24th month. Below are the critical cash flow and returns intel.

The Residual Value of $48,621,390 is calculated by dividing the Year 3 stabilized NOI by a 5.20% residual cap rate.

$2,528,312 / 5.20% = $48,621,390

This would produce an IRR of 79% and an equity multiple of 3.15 at the project level.

Will the stabilized NOI be affected by a future real estate tax increase?

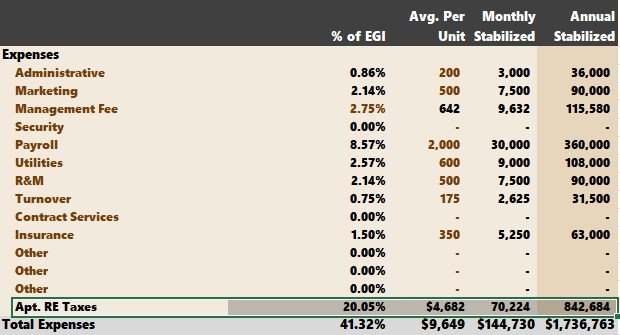

Looking at the proforma expense assumptions, we see that stabilized real estate taxes are projected at $4,682 per unit or $842,684.

This could be a reasonable assumption if the building doesn’t sell. However, it would be prudent to understand how much real estate taxes could increase if the project sells at a higher price than the projected assessment level.

NOI Adjustments

You first need to estimate the forward applicable tax rate. We cannot predict this with certainty, so we assume it will stay the same as the current year at 2.00%.

Then, you’d need to make a reassessment assumption as a percentage of the sales price. It is well known within the investment community in Minneapolis that properties typically reassess between 95%-100% of the purchase price. To be conservative, we will assume 100%.

Let’s see how the Year 3 stabilized NOI would change with a tax adjustment.

“Proforma RE Taxes” is your proforma property tax assumption.

“Reassessment Post-Sale” is the new assessment once the property is reassessed at 100% of the Purchase Price.

“Projected Buyer’s RE Tax Payable” is the new assessment multiplied by the applicable tax rate of 2.00%.

The “Buyer’s RE Tax Exposure” is between $972,428 and $842,684. This delta is the buyer’s NOI loss from a real estate tax expense increase once they take over ownership.

“Adjusted Buyer NOI After Reserves” is the NOI adjusted for the $129,744 real estate tax liability.

The next step is to cap the tax-adjusted NOI of $2,398,568 to see how it affects residual sale proceeds.

The new “Adjusted Residual Value” is $46,126,313, which is $2,495,076 less than what is currently calculated in the proforma for the residual value.

The final step is to examine how this adjustment affects the metrics (IRR and Equity Multiples).

IRR & Equity Multiple (No Tax Adjustments):

Tax-Adjusted IRR & Equity Multiple

If an investor is willing to pay a 5.20% cap rate on the developer’s tax-adjusted NOI, the tax-adjusted cap rate is 5.48%. The decreases in “net proceeds” would cause the IRR to drop from 79% to 67% and the equity multiple to fall from 3.15 to 2.79.

This could trickle into the sponsor’s promote structure and significantly impact the allocation of cash flows between the sponsor and equity partners, especially if the distribution structure is an IRR waterfall.

De-Risking the Proforma

The best potential solution for more conservative development underwriting is to use a tax-adjusted cap rate calculated on the “RE Tax Sensitivity” tab as the residual cap rate on the “Project Summary” tab.

In the underwriting example, we assume a 5.20% residual cap rate in Year 2 when the development sells. Let’s instead use the tax-adjusted cap rate of 5.48% in our proforma.

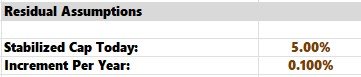

Our current residual cap rate assumptions are the following:

Instead of starting at 5.00%, let’s start at a higher cap rate while keeping the same annual increment of 0.10%. We can “back into” the starting stabilized cap rate today:

5.48% - (0.10% x 2) = 5.28%

In two years, the residual cap rate will be:

5.28% + 0.10% + 0.10% = 5.48%

Having adjusted the residual cap rate to a higher, more conservative, tax-adjusted amount, the proforma is receptive to future tax liability, and the investment metrics showcase this on the “Returns Summary” tab.

Sensible Underwriting

If a developer is sensible with their underwriting assumptions (specifically NOI growth and residual cap rates), the tax liability should dissipate as the investment hold period gets pushed out further. Here’s how it looks in the current model:

As you can see, the delta between the cap rates becomes less material year over year. By Year 10, there is no discrepancy at all.

A lot of this has to do with underwriting being conservative.

Property taxes are increasing by 3% annually

The NOI is growing by 3% annually

The residual cap rate is escalating in 0.10% increments annually

This increase in residual cap rate acts as a governor on the appreciation upside, which limits future property tax liability later in the investment hold.

Summarizing Property Taxes After Sale

The development community must empathize more with investors’ underwriting metrics for the next ownership group. It’s no mystery that developing property in the current environment is becoming more complex with construction costs increasing, competition at all-time highs, rising interest rates, and arguably at the end of a prosperous economic cycle.

Understanding the real estate tax exposure for the next owner can significantly impact the developer’s residual sale proceeds. This understanding may deter more speculative projects from being developed in the first place that are dependent on an overly optimistic residual sales value.