Properly Analyzing Cash-on-Cash Returns in Real Estate Investing

The cash-on-cash return in real estate investment is a misunderstood metric in the real estate industry. Today, I plan on diving deep into the Tactica methodology and how it differs from other calculations you may come across.

Contents

Cash-on-Cash Return Definition

Cash-on-cash in its simplest form, you’d calculate it:

Annual Cash Flow / Total Cash Invested

If you invested $100,000 in an investment property and reasonably expected to earn $6,000 in cash flow after debt service in Year 1, your cash-on-cash return would be 6%.

$6,000 / $100,000 = 6%

Some ambiguity can rear its ugly head when determining what qualifies as cash flow vs. cash invested.

For example:

If you need to pay for a new roof out of pocket, should that be considered a decrease in annual cash flow or an increase in total cash invested (an adjustment to the numerator or denominator)?

If you refinance a mortgage and are fortunate to receive excess cash proceeds, should this be counted as an increase in annual cash flow or a decrease in total cash invested?

Can annual cash flow be considered a reduction in the total cash invested?

Tactica's definition of cash-on-cash return strives to help answer the above questions. The cash-on-cash return does not measure the total return on investment because it is an annual yield.

Yield Metric Cash-on-Cash Return

In the article "A Definitive Guide to Calculating Real Estate Returns," yields are defined as:

"A calculation that demonstrates the performance of an investment over a defined period. Strong yields typically correlate with strong overall investment performance, but not necessarily. Looking at yields alone will give you a snapshot of how the real estate investment is doing in each month, quarter, or year, but can't tell you with certainty the overall investment performance."

Yields won't factor in appreciation and loan paydown, which will have a massive impact on the overall success of the investment. You can realize good cash-on-cash returns annually and still have the investment fail if you can't sell it for more than your purchase.

Another example of a yield is the capitalization rate (cap rate), which takes:

NOI / Purchase Price

Cap rates are a metric to benchmark a property valuation vs. other comparable sales in the marketplace. They’re meant to measure the pricing attractiveness given the historical operations but can’t determine the overall success of an investment.

Good Cash-on-Cash Return

Generally speaking, if the cash-on-cash return is higher than the actual proforma cap rate, you should feel confident in the upside of your potential investment.

Cash-on-Cash Return > True Proforma Cap Rate = Good

With rising interest rates, you’ll commonly hear real estate investors taking on negative leverage in the current investment environment. Negative leverage is when the loan constant exceeds the actual proforma cap rate. In these instances, leverage hurts property yields, and the cash-on-cash return will be lower than the cap rate.

In other words, high pricing and expensive debt wreak havoc on potential returns. Maximizing the cash-on-cash return will hinge on paying below market value for your real estate transaction and improving property management to grow income and cut expenses.

General real estate market knowledge of various asset classes within the submarket will be crucial to best determine reasonable cap rates and cash-on-cash return metrics for a potential investment opportunity.

Total Return Measures

On the other end of the spectrum, metrics that measure total return are:

Internal Rate of Return (IRR)

Annualized Rate of Return (ARR)

These metrics will take into account appreciation and loan paydown and will paint a detailed picture of the overall success of the investment.

Cash-on-Cash Return Formula (Advanced)

The cash-on-cash equation I presented before was oversimplified:

Annual Cash Flow / Total Cash Invested

I want to touch on both the numerator and the denominator.

Numerator: Annual Cash Flow

You can break down annual pre-tax cash flow further into:

Operating Revenues - Operating Expenses - Debt Service

So, annual net cash flow is your recurring revenue, expenses, and mortgage payments. Revenue will be rents, ancillary income, fees, and negative adjustments for vacancies and rental concessions. Recurring costs would be marketing, maintenance (not an improvement), insurance, property taxes, and utilities. Debt service is what you owe the lender each year in principal and interest payments.

Denominator: Total Cash Invested

Total cash invested will be affected by things like:

Unordinary one-time expenses (such as loan origination fees and closing costs)

These items will affect the denominator and be considered total cash invested in the cash-on-cash formula.

Total Cash Invested can be broken down further into:

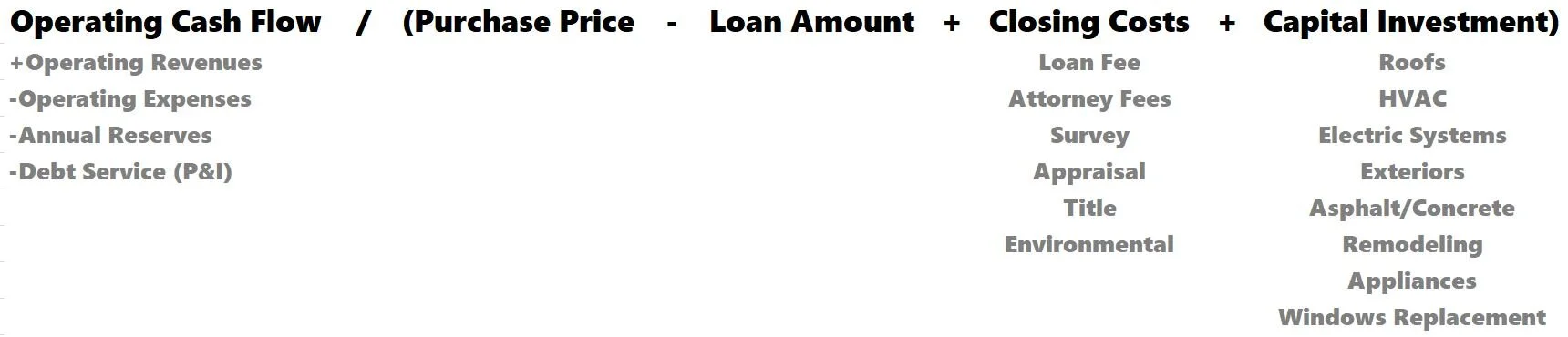

Down Payment + Closing/Loan Costs + Capital Investment

CAPEX will increase the denominator, which means your actual cash investment increases (you increase the total cash basis in the investment). On the flip side, refinance proceeds would reduce your amount of cash in the project (reduce the denominator) because you would get a chunk of your initial investment back.

The image below may help determine how various expense items should be classified.

Categorizing Cash Flows

You may wonder how I determine annual cash flow vs. the total cash invested.

In reality, the IRS determines this. While there may be gray areas when determining how an expense should be classified, any expense that prolongs the life of an investment is typically considered CAPEX. The IRS won't let you deduct 100% of these expenses the year you incur the cost; instead, you must depreciate them over a predetermined number of years.

Spend $100,000 replacing the roof: Your denominator increases.

Spend $55,000 on replacing plumbing fixtures: Your denominator increases.

Raise rents over the past year: Your numerator increases.

Fix the furnace: Your numerator decreases (as long as you didn’t replace the furnace, then the denominator would increase)

Refinance and get $50,000 back of our original $100,000 investment? Your denominator decreases by 50%. The IRS considers a refinance a return of investment principal, not taxable profit.

Disclaimer: Always verify with your accountant how expenses should be classified, as every tax situation differs vastly.

Reevaluating the Cash-on-Cash Yield

The cash-on-cash return metric will be in constant motion from year to year. The numerator and denominator will be in continuous flux. Let's compare two cash-on-cash return examples and see how they change yearly.

Year 1: You make a $500,000 down payment on a rental property. Closing costs and loan origination fees total $7,000, which you'll pay out of pocket. Your project's annual rental income totals $120,000. Operating expenses are projected at $55,000. The loan is interest-only for the first two years, and the interest payment totals $20,000 annually.

Cash-on-Cash Return = ($120,000 - $55,000 - $20,000) / ($500,000 + $7,000)

= $45,000 / $507,000

= 8.98%

Year 2: Rental income increases to $125,000, operating expenses decrease to $53,500, and the interest-only payment is still $20,000 annually. Two water heaters break and cost $2,500 to replace.

Cash-on-Cash Return = ($125,000 - $53,500 - $20,000) / ($507,000 + $2,500)

= $51,500 / $509,500

= 10.11%

Year 3: Rental income increases to $126,700, operating expenses rise to $57,000, and the loan begins to amortize. Debt service is now $28,700. You did a significant landscaping project that cost $7,500.

Cash-on-Cash Return = ($126,700 - $57,000 - $28,700) / ($509,500 + $7,500)

= $41,000 / $517,000

= 7.93%

Let's do another scenario with extensive renovations in the first year.

Year 1: You make a $500,000 down payment on a rental property. Closing costs and loan origination fees total $11,000, which you'll pay out of pocket. You estimate $140,000 in renovation costs to update all the units.

You secured a construction loan that you can draw down during construction. You will pay interest only. You do not expect any cash flow in Year 1, as all units will be vacant while you renovate the property. You will be on the hook to pay interest draw fees and other out-of-pocket holding costs, totaling $33,400 in Year 1.

Cash-on-Cash Return = -33,400 / $511,000

= -6.536%

Property taxes, insurance, and utilities during the renovation will lead to a negative net operating income. There will also be financing costs, leading to negative cash-on-cash yield during the construction Years.

Year 2: You can lease the freshly renovated units and get $144,000 in rental income. Operating expenses will total $67,800. With the property stabilized, you refinance the construction loan into permanent financing. Blowing out the construction loan gives you $420,000 in repayment via refinancing proceeds. Permanent debt coverage costs $34,000 annually.

Cash-on-Cash Return = ($144,000 - $67,800- $34,000) / ($511,000 - $420,000)

= $42,200 / $91,000

= 46.154%

Note: You financed the $144,000 renovations; therefore, the monies spent didn't count as an additional cash investment. If this were an all-cash purchase without financing, you’d add the $144,000 to the denominator.

There's a pretty stark contrast between Year 1 and Year 2. This volatility proves that the cash-on-cash return may not be the best metric for analyzing a capital-intensive project like a fix-and-hold.

Cash-on-Cash Best Uses

The two examples above were meant to lay out two very different investment scenarios where cash-on-cash calculations varied wildly.

Cash-on-cash is a great metric when the purpose of the investment is annual cash flows (preferably predictable) vs. projects banking on forced appreciation.

Cash-on Cash-Effective When Analyzing:

Commercial real estate, such as retail, office, and industrial, will have long-term leases in place and predictable cash flow

Cash-on-Cash NOT as Effective When Analyzing:

Occasionally, the cash-on-cash metric can be helpful on a project with a refinance, but it will never be my go-to annual return metric.

Video: Uncomplicating the Cash-on-Cash Return

Summarizing the Cash-on-Cash Return

Hopefully, you better understand how Tactica calculates the annual cash-on-cash return. It is a yield metric that measures your return over a defined period. This cash-on-cash return is in constant flux when revenues and expenditures are correctly categorized, and you should reevaluate it annually.

The cash-on-case return is helpful when future cash flows are largely predictable and stable. It is less valuable for extensive renovation projects, development, or quick fix/flip projects that expect a significant refinance or sale shortly after closing.