A Definitive Guide to Calculating Returns on Real Estate Investments

There are infinite ways to measure real estate returns; every investor will have unique preferences. This article aims to help you sort through the vast world of real estate return metrics. You'll understand the various calculations and when to use them appropriately.

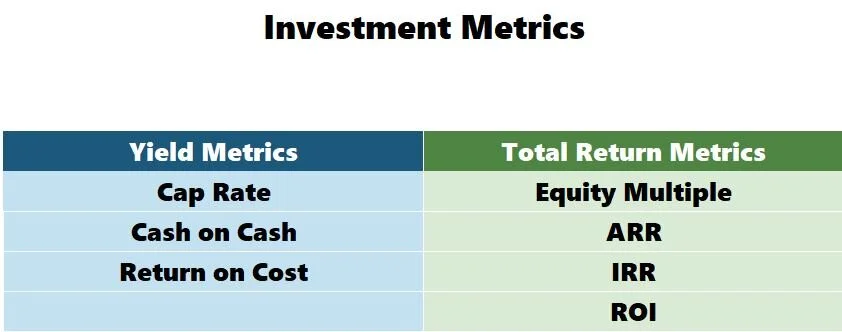

Real Estate Performance Metrics

Defining Your Measurement

You have two options when assessing the return rate for a real estate investment.

Yield

Total Return

Confusion could be eliminated by merely understanding the difference between a yield and a total return. My definitions are the following:

Yields

A calculation that demonstrates an investment's performance over a defined period. Strong yields typically correlate with overall solid investment performance, but not necessarily. Looking at yields alone will give you a snapshot of how the real estate investment is doing each month, quarter, or year, but can't tell you the overall investment performance with certainty.

If you are a stock market investor and buy mutual funds, you may be interested in the fund’s dividend yield. For example, if it has a dividend yield of 2%, you calculate the expected dividend payment each quarter. However, this information alone doesn't disclose the overall investment performance (how much the mutual fund has appreciated or depreciated).

Or perhaps you're a retiree heavily invested in bonds. You select bonds with a coupon payment that will provide enough income to support your lifestyle during retirement. The coupon payment gives you an idea of how safe the investment is, the issuing company's credit quality, and its business strength. The lower the coupon payment, the less perceived risk in investing in the underlying company.

You milk a coupon payment twice a year, but assuming you never went online and checked your bonds, you would have no clue if they appreciate or depreciate in the open market and how that affects your total investment.

In summary, the investment yield is a piece of the puzzle but doesn't paint the entire picture. Depending on your investment goals, this may be sufficient. Yield calculations in real estate investing include:

Capitalization Rate (Cap Rate)

Cash-on-Cash Returns

Return on Cost (ROC)

Total Returns

Total returns paint the entire picture of a real estate investment. They will factor in cash flows from the project, the appreciation, the loan paydown, and the gain on your initial investment. As mentioned above, high yields correlate with higher total returns, but it is not a given. For example, there could be an investment property with fantastic cash-on-cash yields in a terrible part of town that likely won't entice a buyer to pay top dollar when it comes time to sell. While the investor is making a high rental income, selling the property would result in them taking a loss. In this instance, high yield <> high total return.

Total Returns in real estate investing include:

Equity Multiple

Annualized Rate of Return (ARR)

Internal Rate of Return (IRR)

Bonus: You can use Microsoft Excel’s Goal Seek application to “seek out” acceptable yield/return parameters.

Investment Metrics

I visualize Yields and Total Returns in the following diagram:

Yields

Let's begin by defining each of the yields and discussing their purpose and uses.

Capitalization Rate

A cap rate is probably the most commonly used commercial real estate investment metric. A cap rate is defined as:

Net Operating Income / Purchase Price

A cap rate never factors in any capital spending or mortgage payments. It is primarily a qualitative metric used to benchmark a property against comparable sales in a specific real estate market. Cap rates must be taken with a grain of salt as they can be impacted significantly by various operating factors and easily manipulated.

If a broker sends you a "6% cap" deal in a market that traditionally sees "5% caps" at the surface level, you may perceive this as an excellent investment opportunity. You must do much research to determine if this is indeed the case.

The bottom line is that you should use that cap rate very high to compare investments in similar asset classes and verify that the property's value is in line with past sales.

Cash-on-Cash

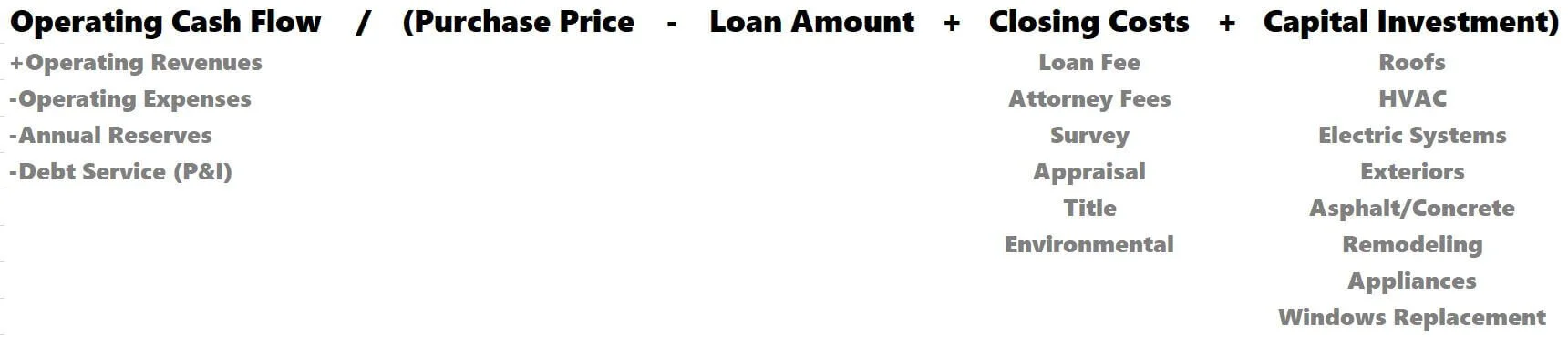

Cash-on-cash is my favorite yield metric and is superior to the cap rate. The cash-on-cash yield factors in capital spending and debt service. Therefore, it is an accurate representation of genuine annual yield. Cash-on-cash yield is calculated by:

Operating Cash Flow / (Purchase Price - Loan Amount + Closing/Loan Costs + Capital Investment )

Operating cash flow is:

Operating Cash Flow = NOI - Debt Service

Let's say a deal costs $10,000,000. Loan origination fees, closing costs, etc., will cost an additional $130,000. You plan on replacing roofs immediately upon taking over the property for $250,000. The loan amount is $7,500,000. Therefore, your total basis in the deal is $2,880,000 (used as your denominator).

You project your proforma year 1 NOI to be $600,000 and annual debt service to cost $456,000. Operating Cash Flow = $144,000

Cash-on-Cash = $144,000 / $2,880,000 = 5.00%

Interestingly, the cash-on-cash is less than the cap rate (cap rate = $600,000/$10,000,000 = 6.00%). I would avoid this deal or negotiate the price because leverage hurts yields compared to buying in cash.

The image below shows different expense items and how they will factor into the cash-on-cash equation.

As you increase operations annually (hopefully) and invest capital back into the property for capital expenditures (CAPEX), the cash-on-cash will be in constant flux. Investors who buy a deal that requires a lot of capital investment will often focus on the cash-on-cash yield in future years once the property is stabilized.

Check out an entire article related to cash-on-cash returns with real-life examples.

Cash-on-Cash with Principal Add-Back

I have seen people use the cash-on-cash and add mortgage principal to the numerator. The rationale is that the principal paydown is equity that should be accounted for. While I agree, I do not think equity, a paper gain, should be considered cash flow. It is a big piece of the IRR calculation, which I will discuss shortly. In the example above, if we included year one principal paydown in the numerator, this hybrid cash-on-cash calculation would be:

$144,000 + $120,992 / $2,880,000 = 9.20%

It's a big difference and can be deceiving. I think it's important to mention this metric as you are bound to run into it if you analyze many real estate deals.

Return on Cost (ROC)

In my experience, the return on cost (or yield on cost) is used frequently in three different ways.

(1) New Construction

Return on cost is a crucial metric in the real estate development world. It is calculated:

Projected Stabilized NOI / Total Construction Cost

If an apartment developer is projecting a stabilized annual NOI of $1,500,000 and the project will cost $23,000,000, the ROC is:

$1,500,000 / $23,000,000 = 6.52%

You can compare the return on the cost to the deal's expected cap rate upon stabilization. The developer would have an upside if the projected stabilized cap rate were 4.50%. $1,500,000/4.5% = $33,333,333.

Assuming they follow through on their business plan and there are no blatant economic shocks, they could sell the deal for over $10,000,000 more than the cost to build.

The higher the delta between the return on cost and the stabilized cap rate, the higher the upside and the less risky the project.

(2) Project Evaluation

I have always used return on cost on existing deals to measure capital investments' performance by taking the potential upside divided by the total cost.

Premium (or Cost Cut) / Total Project Cost

For example, if I want to invest $10,000 into an apartment unit remodel that would return $100 in a monthly rental premium, the ROC:

($100*12) / $10,000 = 12%.

If there were an opportunity to implement LED light fixtures in all common areas that would cost $100,000 and save $20,000 per year in electricity costs, the ROC is:

$20,000 / $100,000 = 20%.

ROC is a great metric when analyzing the financial feasibility of smaller deal components and deciding where and how you want to invest capital. The higher the ROC, the more likely improvements will be accretive to overall investment returns.

(3) Property Repositioning

I’ve also seen an uptick in investors using a return on cost-calculation for capital-intensive real estate projects. Instead of taking a cap rate, they will assess the riskiness of the investment opportunity by factoring in CAPEX spending.

NOI / (Purchase Price + CAPEX)

A cap rate on a project that needs extensive repositioning won’t be an excellent barometer if a CAPEX budget is in the millions. CAPEX items could include:

Boiler replacement

Roof replacement

New siding

Major renovations

New sidewalk

If a $5,000,000 property needs $1,0000,000 in CAPEX and projects a $250,000 NOI, the ROC calculation:

$250,000 / ($5,000,000 + $1,000,000) = 4.167%

That’s a big difference if the broker selling the property was quoting a 5% cap rate.

REIT Metrics

Some yield metrics are used in Real Estate Investment Trusts (REITs) that are important for analysts determining the feasibility of future dividends produced from operating income. Funds From Operations (FFO) and Adjusted Funds From Operations (AFFO) are the most commonly used. These are not GAAP metrics, and the formula can be inconsistent from firm to firm. REIT investment may be the logical option for people with limited funds to make a down payment on a property but still want real estate exposure. You should investigate and understand these two metrics before buying any shares.

Total Returns

We get into total return metrics that measure the overall profitability (or loss). The typical three “total” return metrics are Equity Multiple, Annualized Rate of Return (ARR), and Internal Rate of Return (IRR).

Equity Multiple

The equity multiple is perhaps the least utilized metric in real estate. It is simple, straightforward, and tells an investor precisely what they want to know when analyzing an investment.

Cumulative Distributions / - Initial Investment

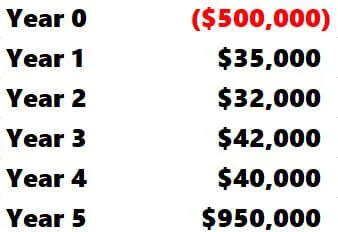

The calculation divides every distribution earned over the investment's life by the initial investment. For example, look at the cash flows below.

In this example, the cash flows' aggregate total in Years 1 - 5 would be added and divided by $500,000.

$1,099,000 / $500,000 = 2.20

Stated differently, investing $500,000 today would double that investment in five years.

I always look at the equity multiple in year seven and see if the equity multiple has achieved 2.00 or higher. If so, the project would return approximately an average of 10% annually during those seven years. In my experience, an aggressive value-add strategy can achieve this. If the equity multiple was significantly higher than 2.00, certain assumptions, such as residual cap rate and rent growth escalators, might be too aggressive.

Annualized Rate of Return (ARR)

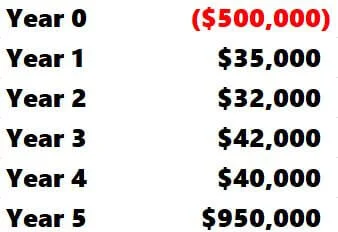

ARR is the same as equity multiple but presented as an annual return. The cash flow we used in the equity multiple scenarios above could be communicated as an annualized return. The formula to convert the equity considerable to an annual percentage is:

Equity Multiple - 1 / Years

In our sample cash flows above, the formula would read:

(2.20 - 1) / 5 Years = 24%

The initial $500,000 investment returned 24% annually each year.

Equity Multiples and ARRs are great metrics for deal sponsors trying to attract investors. The calculations are intuitive and easy to explain. They do have one major flaw. They fail to factor in the time value of money. Equity multiples and ARRs are agnostic about when cash is distributed. All distributions are equal. This can be troublesome for investments where time is of the essence. To combat this, many turn to the internal rate of return.

Internal Rate of Return (IRR)

The IRR is an incredibly complex calculation that appears simple, thanks to Microsoft Excel and other real estate investment technologies. The IRR is the final metric I will cover, and like ARR, it measures total return in the form of an annual return.

I wrote articles about the components of IRR for Existing Projects and New Developments.

IRR acknowledges that cash flows received later in the investment hold aren't as valuable as today’s. The IRR will typically be less than the ARR since most projects see the most significant cash flow distribution upon sale on a future date.

Projects with a refinance early in the investment hold that pays back an investor a substantial portion of their initial investment could see an IRR higher than the ARR. Look at the same cash flows as before and calculate the IRR.

IRR is 18.73%, starkly contrasting the 24.00% ARR previously calculated.

If a significant distribution is made early in the investment hold, the IRR could be higher than the ARR (the net cash flows below are the same as the example above.

ARR is still 23.96%, while the IRR increases to 25.42%. As you can see, timing is everything with the IRR metric.

IRR has its flaws. Investment professionals can manipulate IRR by pulling certain strings to boost an IRR and make an investment appear more attractive. There's also uncertainty in academia about whether it assumes cash flows are truly reinvested at the IRR. This is widely known as the reinvestment fallacy. As a result, some argue that IRR may be overstating returns because cash flows distributed to investors are not being reinvested into the project and are not achieving the IRR. There are online forums with thousands of responses arguing this exact dispute vehemently.

IRR is my preferred metric because it tends to be the industry standard for analyzing real estate. I've examined so many deals focusing primarily on the IRR; it has become a metric that will give me the best sense of investment caliber. I then look at all the other yield metrics to ensure they are reasonable and realistic.

Related: It’s also helpful to compare the “levered” IRR to the “unlevered” IRR.

I would never advise only looking at one metric. Always use them together to form your conclusion. For a more precise measurement of inconsistent distributions, you may consider the XIRR.

Return on Investment (ROI)

The definition of ROI can be tricky, and If you do a Google search on " ROI in real estate," you will see examples of it used as a yield (in a similar fashion as cash-on-cash yield) and as a total return metric (frequently calculating the total return in "fix and flip" strategies). You will need to dive deeper and get further clarification whenever you see an investment described by an ROI metric.

I will use a simple ROI calculation on short-term speculative real estate investments such as a condo or cooperative housing development with no projected recurring investment cash flow. My definition is simple:

ROI = Total Distributions / Total Equity Investment - 1

If you invest $1.5 million and make $2.5 million in distributions, your ROI would be:

ROI = $2.5M / $1.5M - 1

ROI = 67%

Ranking the Five Most Common Real Estate Return Metrics

Summarizing Real Estate Return Metrics

There are multiple ways to quantify the upside of a real estate investment. I like to break up analysis metrics into Yields and Total Returns.

Yields demonstrate an investment's performance over a defined period, while total returns paint the entire profitability picture (or loss). All metrics serve a unique purpose, and all should be considered in tandem when making investment decisions.